Blockchain-Backed Document Verification Points to Faster Real Estate Closings

Accelerate real estate documents with blockchain-backed verification. Discover how secure, tamper-proof records can speed up closings and boost buyer trust.

Blockchain-Backed Document Verification Points to Faster Real Estate Closings

New research into a blockchain-supported real estate document system is shining a light on how the next wave of automation could shrink closing timelines and reduce fraud—especially for independent agents, small brokerages, and solo transaction coordinators who juggle high document volumes with limited back-office support.

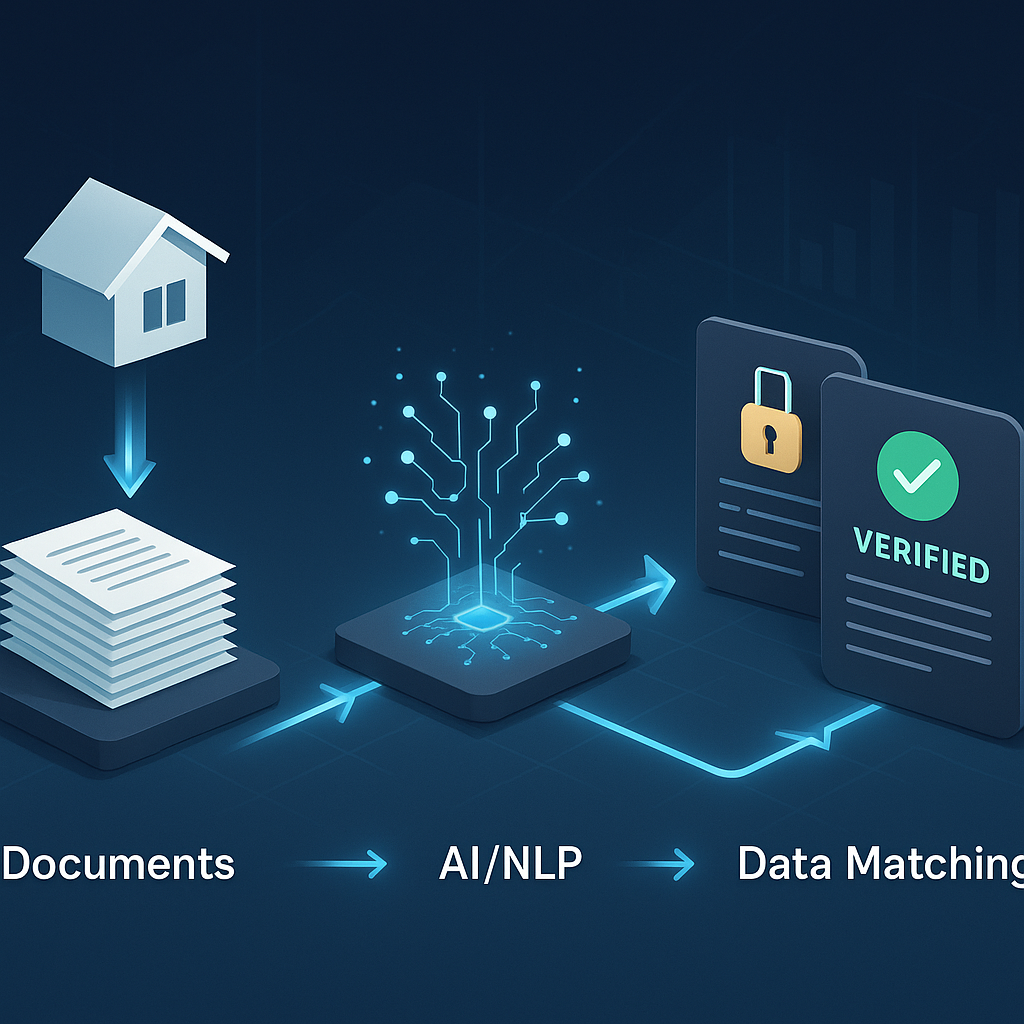

A December 2025 academic study, “Document Data Matching for Blockchain-Supported Real Estate,” proposes a prototype that combines optical character recognition (OCR), natural language processing (NLP), and verifiable credentials (VCs) to automatically extract, standardize, and cross-check data across deeds, IDs, and other closing documents, while anchoring trust on a blockchain network. (arxiv.org)

The emerging model: documents are scanned and parsed by AI, converted into standardized digital credentials, automatically compared for inconsistencies, and then secured with a tamper-evident blockchain record.

Why This Matters for Small Real Estate Businesses

Real estate remains one of the most document-heavy industries. Independent agents, small brokerages, and closing attorneys still spend hours manually reviewing:

- Purchase agreements and addenda

- Deeds and title commitments

- Buyer and seller IDs

- Loan packages and disclosures

That manual review is not just slow—it’s a growing risk vector. Identity and wire fraud targeting real estate transactions continues to rise, with vendors and title organizations responding by rolling out more sophisticated identity verification tools, multi-factor checks, and insured verification workflows. (alta.org)

At the same time, adoption of digital and hybrid closings is steadily increasing, but still far from universal. A survey from the American Land Title Association (ALTA) found that fully digital or hybrid closings reached about 10% of transactions in 2022, up from 7% in 2021, showing clear momentum—but also plenty of room for improvement. (alta.org) More recent lender-focused research shows that even when digital closing tools are available, full adoption often lags due to cost, usability, and process complexity. (businesswire.com)

For small players, that gap is even more acute. Large lenders can fund dedicated teams and custom integrations; solo agents and boutique shops usually cannot. That’s where research into blockchain-backed verification and intelligent document automation becomes particularly relevant: it points toward tools that could eventually offer “big-bank-grade” verification without enterprise-level overhead.

Inside the New Blockchain-Supported Verification Model

Step 1: OCR and NLP Turn Paper into Structured Data

The research prototype starts where many small real estate businesses already are: with PDFs and scans of contracts, IDs, and deeds. An OCR pipeline converts scanned text into machine-readable form, while NLP models identify and label key fields—names, addresses, parcel IDs, closing dates, loan amounts, and more—across heterogeneous document formats. (arxiv.org)

Unlike basic text recognition, the NLP layer is trained to understand the semantics of real estate documents, so it can, for example:

- Distinguish buyer vs. seller vs. agent names

- Extract legal property descriptions and parcel numbers

- Identify risk-relevant fields like wiring instructions or payoff account details

Step 2: Verifiable Credentials Standardize the Results

Once data is extracted, the system converts it into verifiable credentials—a standards-based format for representing claims (such as “John Doe is the owner of Parcel 1234” or “This driver’s license matches the seller”). Those credentials can be issued by trusted parties (title companies, lenders, government entities) and later cryptographically verified by others in the transaction. (arxiv.org)

This standardization is crucial for small businesses. Today, every lender, title company, and local registry seems to have its own PDF format. With verifiable credentials, a small brokerage’s closing platform could interact more easily with multiple partners, reusing the same verified data instead of re-keying the same information over and over.

Step 3: Automated Cross-Checks Flag Inconsistencies

Once documents are represented as structured, machine-readable claims, the system automatically compares them across sources. Examples include:

- Matching seller name and address across IDs, deeds, and contract

- Confirming the property’s legal description is consistent between deed and title commitment

- Verifying that wire instructions are associated with the verified seller or settlement account

According to the research, this automated data matching can flag discrepancies in seconds, while maintaining accuracy levels comparable to manual review. (arxiv.org) Instead of an assistant or paralegal performing a line-by-line comparison, a small office could rely on the system to raise red flags, then have a human double-check only the problematic cases.

Step 4: Blockchain Provides a Tamper-Evident Audit Trail

Finally, the verified credentials—and the logic of what was checked and when—are anchored to a blockchain. In practice, this means:

- Each verified claim (e.g., identity confirmed, deed data matched) is hashed and written to a distributed ledger.

- Any attempt to alter a previously verified document or credential would be detectable, because the hashes would no longer match.

- Participants can independently verify that a given credential or check was performed at a particular time, without needing to trust a

single central database.

For small real estate businesses, this kind of tamper-evident record could strengthen compliance, improve dispute resolution, and offer an additional layer of client reassurance—particularly in remote or high-value transactions.

Real-World Momentum: Identity and Fraud Verification in Closings

While the specific blockchain-backed prototype is still experimental, it is emerging alongside a broader industry push to modernize identity verification and fraud prevention in closings:

- Title and closing vendors are launching seller identity verification solutions that run multi-step checks and sometimes include wire fraud insurance up to $1 million per transaction. (alta.org)

- Closing platforms are expanding identity verification with biometric comparison, KYC checks against non-public data sources, and detailed verification reports aligned with ALTA best practices. (closinglock.com)

- In Canada, integration of bank-verified digital identity credentials into real estate workflows aims to reduce repeated document checks and support AML/KYC regulations while protecting consumer data. (businesswire.com)

In parallel, adoption of digital and hybrid closings is climbing, driven by the promise of faster, more convenient transactions, even though cost, stakeholder buy-in, and technical complexity continue to slow full-scale deployment. (alta.org)

For small brokerages and independent agents, the next frontier is not just e-signing documents—it’s proving those documents, identities, and data points are authentic, consistent, and tamper-evident with minimal manual effort.

What This Means for Small Brokerages, Agents, and Closing Attorneys

For smaller real estate organizations, this research points to several practical implications over the next few years:

- Verification will move earlier in the process. Expect identity and document checks to happen at listing or contract signing, not just at funding. Automated credential-based workflows can front-load risk detection, reducing last-minute surprises.

- Standardized data will matter more than standardized PDFs. Tools that can parse, normalize, and validate key fields across any document format will make it easier to collaborate with multiple lenders and title providers.

- “Trust layers” will become a selling point. Being able to show clients a verifiable history of document checks and identity verification—potentially anchored to blockchain—could become a competitive differentiator.

- Usability and affordability will decide winners. Research prototypes are complex under the hood, but for small teams, the essential requirement is that these capabilities plug into everyday workflows without enterprise pricing or months-long implementations.

How QuickSign Fits Into the Next Generation of Digital Closings

For many small real estate businesses, the first step toward this future is getting out of paper-based, ad hoc document management and into streamlined digital workflows.

QuickSign positions itself squarely in that space as a modern, user-friendly alternative to legacy e-signature platforms—built with small businesses and independent professionals in mind rather than large enterprise legal departments.

From Contract Generation to Signing in Minutes

Rather than starting every transaction by hunting for the “latest” contract template, independent agents and small brokerages can leverage AI Document Generation in QuickSign to create contracts, listing agreements, or NDAs tailored to common scenarios. That helps standardize the upstream inputs that future verification tools—OCR, NLP, and verifiable credentials—will rely on.

Once documents are ready, the workflow is intentionally simple:

- Upload PDF of the purchase agreement, addenda, or disclosures

- Drag & Drop Fields for signatures, initials, dates, and text fields

- Send to buyers, sellers, or co-brokers in a few clicks

Real-time tracking shows when each recipient has opened, viewed, and signed, giving small teams transparency without the need for complex dashboards or custom reporting.

Affordability That Matches Small-Team Realities

Unlike many enterprise-focused solutions that charge per seat, QuickSign offers flat-rate pricing at $15/month for the whole team. That makes it easier for small brokerages and closing shops to give access to assistants, junior agents, and transaction coordinators without worrying about escalating license costs.

There’s also a generous free tier: small teams can test-drive digital workflows with 2 AI document generations and 1 document send to unlimited recipients at no cost, making it low-risk to experiment with e-signature and document automation before fully committing.

Preparing Your Workflow for Blockchain-Backed Verification

Even though blockchain-secured document verification is still in the research and pilot phase, there are steps small businesses can take now to be ready for the shift:

- Standardize your templates. Use tools with AI document generation to reduce variation in your contracts and disclosures; consistent structure makes future OCR/NLP much more accurate.

- Digitize every step you can. Move signatures, addenda, and routine approvals into an e-signature platform so there is a clear, timestamped record of each action.

- Adopt basic verification best practices today. Even before full verifiable credential systems are mainstream, incorporate ID checks, call-back procedures, and clear documentation for wiring instructions.

- Choose tools that play well with others. As verifiable credential and blockchain standards mature, open, API-friendly platforms will be best positioned to integrate identity, document, and signing data into a single, cohesive record.

The future of digital closings is not just faster signatures—it’s a fully verifiable chain of trust from the first ID scan to the final wire confirmation, accessible even to the smallest brokerage.

E-signature platforms that are already helping small businesses streamline documents—like QuickSign with its AI document generation, drag-and-drop sending, real-time tracking, and flat-rate pricing—serve as a practical on-ramp to that future. By digitizing and standardizing today’s workflows, they make it easier to plug into tomorrow’s blockchain-backed verification layers as they move from research labs into production tools.

Looking for an affordable e-signature solution? Try QuickSign for free - no credit card required.